What is an Endorsement Split Dollar?

(And how can it benefit your organization?)

IRC 61-22: Under Endorsement Split Dollar, the employer owns the life insurance policy. The employer “endorses” to the executive the right to name the beneficiaries of all or a part of the death benefit – typically being the total death benefit minus the greater of the cash value or cumulative premiums paid. The executive pays income tax annually based on this share of the death benefit, which is known as the economic benefit cost. Typically, a “roll-out” or transfer of policy ownership takes place once an executive reaches a certain access date. Once this transfer occurs, the executive is taxed on the greater of the cumulative premiums or cash value as W2 income, which is subject to IRC Section 4960, which imposes a 21% excise tax for any compensation paid above $1M.

Endorsement split dollar plans are designed to provide valuable key person death benefits to an employer and personal death benefit protection to a key employee's family. A life insurance policy is purchased, and the premium payments and policy benefits are divided between two parties—usually a business and an employee.

How It Works

In an employer sponsored split dollar plan, sometimes called an economic benefit regime, an employer provides the benefits of a life insurance policy to a key employee by splitting the value of the policy between the employee and the company.

Under this arrangement, the employer owns the policy, pays the premium, and retains all rights to the cash values for the length of the employee’s agreed-upon tenure. The employer endorses a portion of the policy’s death benefit to the employee to ensure that his or her beneficiaries receive financial support in the event of his or her death. However, the business retains control over the policy and its cash values. The key employee pays taxes on the value of the life insurance protection, called the reportable economic benefit charge (REBC), each year.

Applicable

Businesses that implement a split-dollar life insurance arrangement must comply with Section 101(j) of the Internal Revenue Code (IRC), which applies specifically to corporate-owned life insurance policies. The Code sets specific record keeping and reporting requirements and sets limits on the amount of premiums that can be paid by the business.

Organization Perspective

- The employer pays the premiums

- May access the policy cash value

- Typically receives the greater of the cash value or cumulative premiums upon death of the executive

Executive Perspective

- Selects beneficiaries

- Receives cost effective death benefit coverage, as the employer typically grosses-up the imputed tax cost associated with this arrangement

- Typically, upon an access date, the policy ownership is transferred to the executive, whereas the executive will owe ordinary income tax on any amount that is transferred

Key Considerations

- Retention Value

- Timing and Amount of Capital Requirements

- Impact on Financial Statements

- Flexibility

- Plan Administration Requirements

- Regulatory Environment

- Taxation

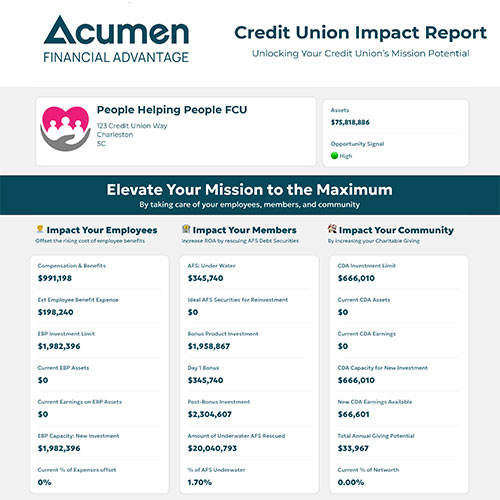

Want to learn how your credit union can maximize its mission across employees, members, and community? Complete the form below, and we will send you a customized Impact Report highlighting opportunities to reduce costs, improve ROA, and expand charitable giving — helping you elevate your mission to the maximum.

We'd love to help you and your team navigate the complex plans, limitations and opportunities. Complete the form below and we'll invite you to a free consultation.

Explore Our Solutions

Discover how Acumen Financial Advantage helps organizations strengthen financial performance, reinforce leadership continuity, and steward resources for long-term value—building durable advantage in service of those you support.