What is a Super Roth Life Insurance Policy?

(And how can it benefit your organization?)

A Super Roth Life Insurance ( Super Roth LI) policy is a specially designed life insurance policy focusing on cash accumulation and tax-free retirement income. Whether it is a dividend paying whole life or universal life, the policy is structured to maximize the living benefits to the policyowner.

What Makes a Super Roth LI policy different from the run of the mill policy? Design. Not all life insurance policies are structured with the correct intent. Most focus on the death benefit aspect, which increases internal costs, leaving the inside cash build inefficient. Our policies are designed to keep the internal costs as low as possible, thus allowing the internal inside build-up to grow effectively and efficiently over time. These plans are funded with after-tax funded dollars, and the inside build-up grows tax deferred and can be accessed tax-free while living.

Key Benefits to Employees:

- Tax-Free Growth and Access to Funds: The cash value within the Super Roth LI grows tax-deferred and can be accessed tax-free.

- Diversification of Policy Type: There are two applicable policies

- Whole Life: Which offers steady consistent non-correlated growth of the cash values through an insurer's guarantees and dividends.

- Universal Life: Which offers two different structures

- Separate Accounts: Similar to other investments, you can choose funds based on risk profile and time horizon. These policies require active management as you may lose value. That said, they offer the most upside potential.

- Indexed Life: Cash value growth mirrors external equity index, but protects your values from loss through a guaranteed return (floor) of typically 0%. The trade off for this guarantee is the upside is limited by a cap, anywhere from 10-15% depending on the year.

- Supplemental Retirement Income: Policyowners can access the cash value at any point, providing a flexible source of liquidity and tax-free income. However, the policy must be adequately funded and properly managed to avoid lapsing or triggering tax consequences.

- Death Benefit for Family Security: The policy includes a death benefit, ensuring financial support for the employee’s beneficiaries.

- Customizable and Flexible: Super Roth LI policies offer flexibility in premiums and benefit amounts, which can be tailored to individual circumstances and financial goals. Whole life is slightly less flexible than the universal life cousins, but does offer more stability.

Key Benefits to Tax-Exempt Organizations

- Attractive Executive Retention Tool: Super Roth LIs can serve as a valuable retention tool as not all providers are familiar with structuring life insurance policies in this manner, nor may they have access to the proper insurance carriers. There are also instances where the employee may not have to go through a typical underwriting process, so long as enough people sign up.

Applicable Codes

- IRS Code Section 7702: Proper structuring under Section 7702 ensures that the policy retains its tax-advantaged status. Failure to comply could result in the policy being treated as a Modified Endowment Contract (MEC), which alters its tax treatment.

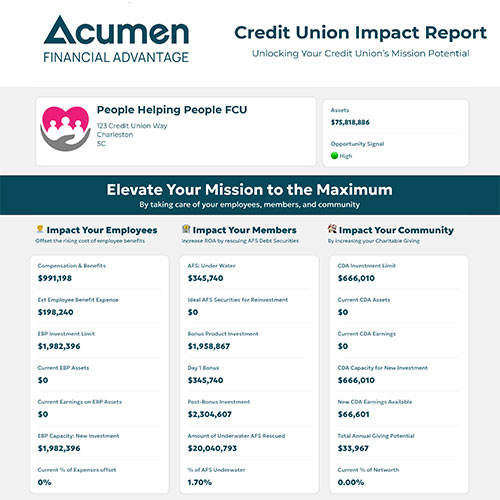

Want to learn how your credit union can maximize its mission across employees, members, and community? Complete the form below, and we will send you a customized Impact Report highlighting opportunities to reduce costs, improve ROA, and expand charitable giving — helping you elevate your mission to the maximum.

We'd love to help you and your team navigate the complex plans, limitations and opportunities. Complete the form below and we'll invite you to a free consultation.

Explore Our Solutions

Discover how Acumen Financial Advantage helps organizations strengthen financial performance, reinforce leadership continuity, and steward resources for long-term value—building durable advantage in service of those you support.